Compound · Issue 05 · Free

The corridor filings will show late

US 380 is not interesting because it is growing. It is interesting because the public record already shows the sequence before the clean filings arrive.

—

A REIT filing is clean because it is late.

By the time a corridor shows up in acquisition commentary, same-store rent language, development pipeline tables, or a market footnote, the messy local work has already happened. The road alignment moved from rumor to public document. The city updated its plan. The school district started talking about boundary pressure. The water line moved into the capital budget. The grocer opened. The hospital announced. The permit portal changed. The tax base caught up later.

That is the useful thing about US 380.

Not that it is a hot North Texas corridor. That sentence is too vague to underwrite. North Texas has dozens of hot corridors, and most of them can support a booster map if the arrows are thick enough.

The better claim is narrower: US 380 is a worked example of how a corridor becomes institutionally legible before institutional filings make it easy to see. The local record sits across TxDOT project pages, environmental documents, city budgets, school bond sites, development dashboards, agenda packets, county subdivision rules, appraisal rolls, utility plans, and retailer releases. It does not arrive as one dataset. That is the point.

The investor who waits for the clean dataset is outsourcing the first read to someone else.

The old way is clean, useful, and late

The clean way to read a market is to wait for clean sources.

A public REIT says North Dallas is strong. A broker deck shades the growth corridor. A quarterly supplemental shows development pipeline by market. A data vendor reports supply, rent growth, absorption, and cap rates. A fund update says the sponsor likes the path of growth.

All of that is useful. None of it is early.

It also compresses too many stages into one word: growth. A corridor can be growing because rooftops are arriving. It can be growing because a road is environmentally cleared but unfunded. It can be growing because schools are behind. It can be growing because a hospital follows young families. It can be growing because an employer makes weekday demand less residential. It can be growing because land basis already moved faster than rents can justify.

Those are different facts. They create different underwriting conclusions.

For an allocator, the useful question is not “is US 380 growing?” It is:

Which public signals tell me this corridor is moving from local/private formation into institutional asset pricing?

That question requires a different reading stack.

The local signal stack

A corridor forms in layers.

First, the physical corridor has to be plausible: alignment, frontage, interchanges, ROW, grade separations, and the environmental process that turns a line on a map into a public decision record.

Second, the civic layer has to absorb the growth: comprehensive plans, overlays, zoning, plats, ETJ handoffs, county subdivision rules, school capacity, utility relocations, water and wastewater capacity, power infrastructure, and public finance.

Third, the market layer starts to confirm demand: rooftops, grocers, big boxes, hospitals, employers, destinations, permits, certificates of occupancy, and appraised values.

Fourth, the institutional layer finally arrives: transaction comps, stabilized NOI, public-company commentary, portfolio marks, acquisition pipelines, and development yields.

The lag is not a bug in the filing system. It is the natural order of the process.

Here is the US 380 stack. None of these facts alone is the thesis. The thesis is the alignment among them.

| Layer | What the public record already shows | Allocator read |

|---|---|---|

| Road | TxDOT’s Collin County feasibility work began in 2017 and was completed in 2020; the McKinney FEIS/ROD selected the Blue Alternative in 2023; Prosper/Frisco received a FONSI in 2023; Denton’s interim grade separations were marked complete in 2026. | The corridor is not just a future arrow. It has moved through multiple public gates. |

| Dollars | TxDOT’s Q1 2024 breakout sheet listed roughly $7.97 billion across five US 380 project buckets: Prosper/Frisco, McKinney, Princeton, Farmersville, and Denton/Collin. | This is allocator-scale public capex before private income statements catch up. |

| H3 corridor proxy | A geostack pass around a 3-mile public corridor proxy — US 380 / University Drive plus the growth-frontier segments of Preston Road and US 75 / Central Expressway north of 380 — shows the corridor-buffer H3 set moving from about 307,000 people in 2010 to 549,000 in 2023, workplace jobs from about 84,000 to 152,000, and aggregate household income from $7.6 billion to $26.5 billion. | This is not parcel proof. It is a cleaner way to ask whether the growth is in the corridor catchment rather than merely in the metro story. |

| Schools | Prosper ISD’s 2023 bond program was $2.7 billion; Celina ISD materials describe more than 7,000 expected new students over five years; McKinney ISD shows northern-zone pressure and 17,339 future lots in a 2Q25 housing report. | Schools are often the first operating system to admit the rooftops arrived. |

| Utilities | McKinney’s FY2025-26 budget includes more than $330 million of FY CIP funding, more than $2.2 billion over five years, and a US 380 Utility Relocations project. Prosper’s FY2025-26 budget includes a $17.1 million US 380 water/wastewater relocation. NTMWD and Oncor/PUCT records show regional capacity moving through public approvals. | Roads do not make a corridor investable by themselves. Utilities are the diligence seam. |

| Commercial anchors | H-E-B, Costco, Target/Gates, PGA Frisco, Universal Kids Resort, Cook Children’s, Children’s Health, Methodist Celina, Raytheon/RTX, and Prysmian/Encore Wire have source-separated support, with the caveat that some are rooftop-serving retail, some are healthcare/service anchors, and some are employer or destination gravity. | Separate rooftop-following retail from true employer and destination gravity. |

The table does not say “buy land on 380.” It says the public information stack is already richer than the filing stack.

The geography is no longer hand-wavy

Citywide growth tables are blunt instruments. They are useful for context, but they cannot tell you whether the corridor catchment changed or whether you are just narrating the metro.

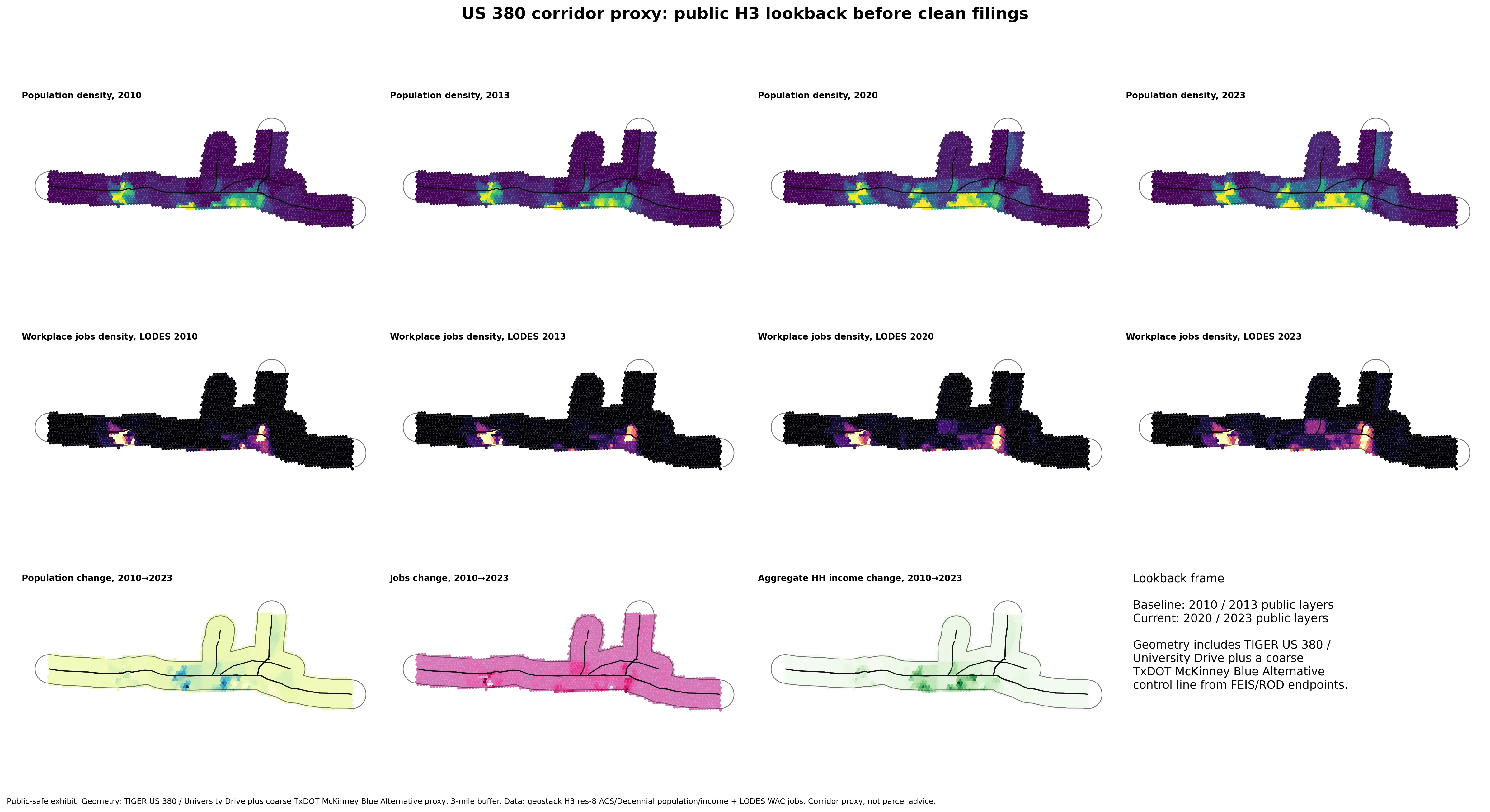

So I built a public-safe H3 exhibit using the same geostack pattern from Issue 04. The frame is a lookback: 2010 / 2013 public layers versus 2020 / 2023 public layers.

380 itself, though, is mostly a retail and commercial corridor. The households follow the north-south arteries that cross it — Dallas North Tollway, Preston Road, and US 75 / Central Expressway — not the east-west highway. So the exhibit geometry is 2024 Census TIGER road centerlines named US Hwy 380 / University Drive in Collin and Denton counties, plus a coarse TxDOT McKinney Blue Alternative control line based on FEIS/ROD endpoints from Coit Road to FM 1827 / New Hope Road, plus Preston Road and US 75 / Central Expressway — each clipped to only the segment north of its own crossing with US 380, so the exhibit isolates the growth frontier (Prosper, Celina, north McKinney) rather than diluting it with already-mature Frisco and Plano to the south. Dallas North Tollway drops out of that north-of-380 slice entirely: the current public road record shows it physically ending near US 380 in Prosper, with Preston Road carrying the corridor north from there. The combined public route proxy is buffered by three miles and intersected with H3 resolution-8 cells.

It is not final TxDOT engineering geometry. It is not a parcel screen. It is not an owner list. It is a corridor-catchment proxy.

Within that proxy, the public datasets move enough to matter:

| Corridor H3 proxy | 2010 | 2013 | 2020 | 2023 | 2010→2023 change |

|---|---|---|---|---|---|

| H3 cells | 1,867 | 1,867 | 1,867 | 1,867 | — |

| Population | 307,092 | 322,259 | 502,336 | 549,035 | +241,942 / +79% |

| Workplace jobs | 84,394 | 85,699 | 122,529 | 152,371 | +67,978 / +81% |

| Resident workers | 110,752 | 143,090 | 222,771 | 278,867 | +168,115 / +152% |

| Occupied units | 95,722 | 107,088 | 150,659 | 183,236 | +87,514 / +91% |

| Aggregate household income | $7.6B | $9.4B | $17.9B | $26.5B | +$18.8B / +246% |

The exhibit does not prove that any specific site works. It proves something narrower and more useful: the “US 380 is growing” sentence can be tested against a consistent public corridor proxy — one built around where the rooftops actually sit, not just the retail spine — instead of waved through with a metro map.

The road record is past the rumor stage

The road record matters because it is the spine everything else hangs on.

TxDOT’s Collin County US 380 feasibility study began in 2017. TxDOT says the countywide study was completed in 2020, and the corridor was then separated into independent project segments. That segmentation matters. If you wait for one giant “US 380 project” filing, you will miss the actual public record because the corridor is moving as a chain of CSJs, environmental reviews, schematics, ROW steps, and funding windows.

The McKinney segment is the strongest example. TxDOT’s approved Final Environmental Impact Statement and Record of Decision, dated September 2023, selected the Blue Alternative for US 380 from Coit Road to FM 1827. The selected alternative is an eight-lane freeway, primarily on new location, around north McKinney. The document ties need to population growth, traffic volumes exceeding existing capacity, congestion, reduced mobility, and higher crash rates.

That is a different signal than a broker saying “north McKinney is growing.”

The Prosper/Frisco piece is also visible. TxDOT’s public-hearing materials for US 380 from Teel Parkway/Championship Drive to west of Lakewood Drive list a 2026 anticipated ready-to-let date and an $890 million estimated construction cost, while also saying the project was then unfunded and could not let until funding was identified. The FONSI followed in July 2023.

That gap between environmental/design readiness and funding/letting readiness is not dead time. It is where local actors start behaving as if the future road exists while the clean capital-market record still looks incomplete.

Denton County gives the execution bookend. The interim grade-separation work from Loop 288 to west of CR 26 had TxDOT letting/start dates in 2020-2022, and Denton County marked the project complete in June 2026 at a reported $160.6 million cost. Meanwhile, the broader Denton feasibility record still contemplates limited-access alternatives.

So the road story is not “someday TxDOT may do something.” It is feasibility, environmental clearance, selected alternatives, public cost boards, utility relocation planning, funding gaps, delivered interim improvements, and future segment windows all at once.

That is how local formation looks before it becomes clean.

Schools and permits show the operating strain

Population headlines are easy to misuse. School documents are harder to wave away because school districts have to operationalize rooftops: redraw boundaries, buy land, borrow money, build seats, and explain why one side of the district is over capacity while another side is not.

The Census Bureau’s Vintage 2025 estimates put Celina, Prosper, McKinney, Frisco, and Little Elm at 645,715 people, up about 149,800 from 2020. Those are place estimates, not corridor catchments, but they explain why the school documents are loud. Prosper ISD’s 2023 bond program authorized $2.7 billion. Celina ISD expects more than 7,000 new students over five years. McKinney’s EFAC material points to pressure in the northwest and northeast regions while some southern areas have different utilization dynamics.

That nuance matters. The corridor is not a circle expanding smoothly. It is an uneven set of pressure points.

Permits have the same problem. Most market screens treat building permits as an early indicator. They are early compared with stabilized NOI. They are late compared with comprehensive-plan updates, overlay districts, TIRZs, zoning cases, plats, infrastructure agreements, ETJ handoffs, drainage review, utility-capacity review, and TxDOT access conversations.

Frisco and McKinney are comparatively usable. Prosper has useful public layers, but extraction is harder. Little Elm and Celina are more case/portal/agendas than clean longitudinal reports. Denton and Collin counties matter where city limits, ETJs, OSSF, floodplain, culvert, subdivision, and county development services intersect.

That fragmentation is not a research annoyance. It is the information edge.

A national allocator pulling only aggregate permit totals will miss the early public pipeline. A local process sees the sequence before the permit count does.

Bonds are not vibes. They are the public balance sheet admitting the rooftops arrived.

Utilities are the diligence seam

A road corridor is not automatically a development corridor.

You still need water, wastewater, power, drainage, pump stations, utility relocation, and local capital capacity. This is where many growth stories get lazy. They assume the line on the map creates the project. It does not. It creates a utility question.

McKinney’s FY2025-26 budget is the cleanest current city-dollar anchor. The budget shows more than $330 million of FY CIP funding and more than $2.2 billion over five years. It includes US 380 Utility Relocations, project C02416, with large amendment and FY/future-period line items.

Prosper adds a west-corridor utility example: a named US 380 30-inch water / 8-inch wastewater line relocation, budgeted at $17.1 million total, plus water/wastewater CIP growth from $45.8 million in the FY2022-23 five-year table to roughly $181 million in the FY2024-25 and FY2025-26 budget tables.

The regional layer says the same thing at larger scale. NTMWD’s public record shows Leonard Water Treatment Plant operating on Bois d’Arc Lake water in 2023, master-planned to 280 MGD, with late-decade Texoma conveyance moving through budget, committee, and board records. PUCT Docket 53053 approved Oncor’s Ivy League 138-kV line and substation in Collin County in December 2022, tying the project to Princeton-area reliability issues, projected overloads, more than 3,400 requested new residential connections, and nearby large-load requests.

The point is not the exact line item. The point is that city budgets, water-board packets, and utility-regulator dockets are converting the transportation and rooftop story into water, wastewater, and power work.

This is where I would spend the diligence hour.

Not “is the corridor growing?” but “which segment has road, water, sewer, power, school, and permit sequencing that can actually absorb the growth?”

If the answer is yes, the public filings will show late. If the answer is no, the road map is just a more expensive broker arrow.

Retail confirms; employers and destinations change the question

Retail is the easiest layer to overread.

H-E-B is real evidence. The company opened its second Frisco store at Highway 380 and FM 423 in August 2024: 130,000 square feet and more than 700 partners. It then opened the Prosper store in August 2025 at Frontier Parkway and the Dallas North Tollway: 133,000 square feet and 570 partners.

Costco and Target make the Prosper sequence more useful because the public record is not just a ribbon-cutting. Prosper EDC announced Costco at FM 1385 and US 380 in April 2023. Town development records later listed a Costco Warehouse permit at 5620 West University Drive with 160,549 square feet and $18.9 million of value. Town and state records put Target at Gates of Prosper into a similar public sequence: TDLR project filing, Town certificate of occupancy, then the operating store page. The exact Target opening date and jobs number remain local-media reported, not official-primary-source verified.

Those are hard signals, but they are mostly rooftop-serving signals. A grocer or warehouse club does not casually underwrite that much store and labor into a weak household market, but retail mostly confirms the demand surface. It does not necessarily create the primary employment gravity.

The stronger non-retail signals are different. PGA Frisco and Universal Kids Resort are destination-gravity signals. Cook Children’s, Children’s Health, and Methodist Celina are healthcare and family-service signals. RTX/Raytheon and Prysmian/Encore Wire in McKinney are skilled-employment and industrial-supply-chain signals, though they should be described as McKinney-area gravity rather than direct US 380 frontage unless a separate source supports frontage.

A corridor made only of rooftops and grocery stores is one kind of investment question. A corridor with rooftops, groceries, hospitals, destinations, and skilled employers is another.

The underwriting mistake is to call both “growth” and move on.

What filings will eventually show

If this sequence keeps moving, the clean filings will eventually catch up.

You will see more north-corridor language in public-company commentary. You will see development pipelines named more cleanly. You will see stabilized assets trade with better comps. You will see taxable values, sales-tax receipts, and permit summaries that make the historical case look obvious. You will see broker maps redraw the edge of the “real” market after the local work is already done.

That does not mean every project works. It does not mean land basis is cheap. It does not mean the right answer is to own anything on the corridor. In fact, one of the risks is the opposite: the public facts can be right while the private price is already wrong.

The job is not to cheer for US 380. The job is to understand where the public sequence is ahead of the institutional record and where the capital stack has already capitalized it.

In CRE, “early” rarely means secret. It often means public, fragmented, boring, and not yet packaged.

What would change my mind

There are several ways the US 380 thesis can be wrong.

TxDOT could delay or de-scope the key segments. If the major project buckets slip materially, lose funding priority, or change scope, the corridor still grows, but the controlled-access conversion story weakens.

Utilities could become the binding constraint. Water, wastewater, pump stations, wholesale supply, power, and utility relocation timing can turn road certainty into development delay. McKinney, Prosper, NTMWD, and PUCT/Oncor now have stronger public-record evidence, but the question remains whether capacity is sequenced fast enough by segment.

The geography could still be too broad. The H3 exhibit is better than citywide data because it uses a consistent 3-mile public-route proxy, and better still because it follows the north-south household corridors rather than just the 380 spine. It is still a proxy, not a final TxDOT preferred-alignment buffer or parcel-level catchment — and the north-of-380 clip point for Preston Road and US 75 is a judgment call, not an official jurisdictional line.

Schools could over-project. Rates, builder starts, student yield, age-restricted housing, private/charter share, or delayed bond implementation could reduce the capacity pressure.

Retail could cannibalize. H-E-B, Costco, and Target can shift spending from older nodes as well as validate new ones. Store openings are not the same thing as net new demand.

Land basis could already be ahead of the evidence. A public signal is not automatically a mispriced signal. Sometimes the local market capitalized it years before the public analyst noticed.

Those risks do not kill the method. They define the next diligence questions.

The actual use case

This is the practical rule I would take from US 380:

Do not start with the filing. Start with the sequence.

For any corridor, ask:

- What is the road or access change, and where is it in the public process?

- What did the city, county, and school district do before the building permit?

- Which utilities and public capital projects make the next phase physically possible?

- Which retailers are following rooftops, and which employers or destinations are creating demand?

- Which data is clean, which is fragmented, and which is missing because the process has not reached that layer yet?

- What price has already moved?

That last question keeps this from becoming boosterism. A corridor can be real and still not be cheap.

The filings will show late. The broker maps will look clean after the fact. The local record will be annoying the whole way through.

That is why it is useful.

—

Compound is a bi-weekly Monday letter on bottom-up CRE analysis, informed by operator-grade private-market context. Free bi-weekly, with paid deep-dives launching later in 2026. Subscribe at matthewd.com/letter.

—

Methodology + sources

Research packet: This draft is based on sources/external/2026-07-07-sh-380-corridor-research.md, which consolidates the 2026-07-07 crawler batch for TxDOT/infrastructure, permits/jurisdictions, rooftops/schools, retail/employer signals, land/public-dollar analysis, utilities/CIP, and internal H3/geostack assets.

Transportation: TxDOT / Keep It Moving Dallas US 380 project pages; US 380 McKinney FEIS/ROD approved September 2023; Prosper/Frisco FONSI and public-hearing boards; US 380 breakout project sheet, Winter / Q1 2024; Denton County June 23, 2026 completion notice for US 380 interim grade-separation work.

Population and H3 exhibit: U.S. Census Bureau Vintage 2025 Texas subcounty population estimates; geostack output at /Users/matthewdickson/projects/geostack/outputs/msa_gravity/us380_h3/us380_wide_north_h3_evolution_panel.png and us380_wide_north_corridor_h3_timeseries.csv (published copy at /letter-assets/issue-05/us380_wide_north_h3_evolution_panel.webp). Geometry is a public TIGER route proxy — US 380 / University Drive plus a coarse TxDOT McKinney Blue Alternative control line from FEIS/ROD endpoints, plus Preston Road and US 75 / Central Expressway clipped to the segment north of each road’s own crossing with US 380 — buffered three miles. Dallas North Tollway is excluded from the north-of-380 slice because the current TIGER road record shows it ending near that crossing. It is not final TxDOT engineering geometry or parcel-level screening, and the north-of-380 clip point is an editorial judgment call, not a jurisdictional boundary.

Schools / permits / public finance: Prosper ISD 2023 Bond Program; Celina ISD Bond 2025 pages and February 13, 2024 demographic report; McKinney ISD EFAC page and linked 2Q25 demographic/housing report; Frisco, Prosper, McKinney, Little Elm, Celina, Collin County, and Denton County official permit/planning/agenda/development-service pages; Town of Prosper FY2024 ACFR; City of Princeton FY2024 ACFR; City of McKinney FY2024 ACFR; Collin CAD reports landing page.

Utilities / CIP: City of McKinney FY2025-26 annual budget and CIP; Prosper FY2022-23 through FY2025-26 budgets and FY2024/FY2025 ACFRs; TxDOT FEIS/ROD utility-relocation discussion; NTMWD Leonard WTP / Bois d’Arc / Texoma Two-Step project pages, FY26 budget summary, committee packet, and board minutes; PUCT Docket 53053 / Oncor Ivy League final order.

Commercial anchors: H-E-B newsroom releases for Frisco Highway 380/FM 423 and Prosper Frontier/DNT; Prosper EDC and Town reports for Costco; Target/Town of Prosper/TDLR records for Gates of Prosper; City of Frisco/PGA/Universal sources for PGA Frisco and Universal Kids Resort; Cook Children’s, Children’s Health, Methodist, Raytheon/PRNewswire, Prysmian, and MEDC sources for healthcare and industrial anchors. Numeric job counts are used only where primary/company/city sources support them.

Internal/private boundary: No parcel-specific recommendation, owner targeting, lead list, private score, or gridx operator map is used here. Internal H3/geostack and gridx/plat-land assets support methodology only. Any public exhibit should aggregate to corridor/H3/civic layers and cite public sources.

What this is not: Investment, tax, or legal advice. A recommendation to buy, sell, lease, finance, or develop any specific property or security. Local real asset intelligence is a screening and diligence framework, not a substitute for site visits, lease review, zoning diligence, environmental work, survey, title, engineering, financing diligence, or local market calls.